The IC view of the gambling sector

Gambling companies have been among the winners of the pandemic as people have looked for a distraction from the boredom of repeated lockdowns. While there has been pressure from the cancellation of sporting events and closure of casinos and betting shops, this has been tempered by consumers flocking to online and mobile betting.

Indeed, for Ladbrokes-owner Entain (ENT) – formerly known as GVC – while underlying cash profits (Ebitda) from its retail operations dropped by close to two-thirds last year, to £98m, profits from its online businesses jumped by 50 per cent to £804m.

Online gambling was already on the rise pre-pandemic as the smartphone era has, effectively, put a casino in everyone’s pockets. But growth has been turbocharged over the past year, and this has been reflected in the momentum of many UK gambling stocks. For example, 888 Holdings’ (888) share price is almost 150 per cent higher than at the start of last year.

The recovery of share prices to above pre-pandemic levels also displays investors’ enthusiasm for the growth potential of the US market, as more states legalise sports betting and internet gambling. UK-listed companies such as Flutter Entertainment (FLTR) have been making considerable headway across the Atlantic, although domestic names are looking to catch up.

Wall Street is also piling into gambling stocks, and Penn National Gaming (US:PENN) and Caesars Entertainment (US:CZR) found themselves promoted to the S&P 500 index last month.

Heading into the pandemic, the shares of UK-listed gambling companies had been weighed down by the spectre of increasing regulation in more mature markets, such as the UK and Australia. Governments have been looking to reduce the risk of gambling addiction and potential exploitation of vulnerable members of society, including children.

That regulatory threat hasn’t abated, particularly as the UK undertakes a review of its gambling laws. The 2005 Gambling Act was designed to regulate an industry that was largely reliant on physical betting shops, but as gambling has shifted online, culture secretary Oliver Dowden says that it is “an analogue law in a digital age.”

Changes could see curbs on advertising – such as a ban on football shirt sponsorship – as well as limits on online stakes and spending. This follows the maximum stake on fixed odds betting terminals (FOBTs) in brick-and-mortar shops being slashed from £100 to just £2.

Betting has become almost synonymous with football as two-fifths of Premier League teams have their shirts adorned with the logos of gambling companies. A report published last year by a House of Lords select committee recommended that gambling operators should not be allowed to advertise in or near sports venues, or on any part of a sports team’s kit. In acknowledgment that this might have a greater impact on smaller football clubs, it said that these restrictions should not be implemented for teams below the Premier League before 2023.

There could also be increased scrutiny over how gamblers’ data is being used as companies collect everything from behavioural patterns to financial information. Targeted promotions based on this data could be encouraging ‘loss-chasing’ – continuing to bet in order to try to recoup losses – keeping customers hooked.

The Treasury is unlikely to want to come down too hard on the industry as it is a source of tax revenue, although a report by think tank the Social Market Foundation (SMF) suggests that stricter gambling laws could actually increase the government’s tax haul. The SMF estimates that if net spending on gambling fell by around £1bn, tax revenue would increase by £171m, as consumers shift their spending to areas such as retail, which have longer supply chains and generate more taxes for every pound spent.

Entain is attempting to get ahead of the regulatory curve – the group announced at the end of last month that it will roll out player affordability checks and individual stake limits by the summer of 2021, focusing on “vulnerable, or particularly at risk” customers.

But some argue that excessive regulation could prove counterproductive. Jason Ader, co-founder and chief executive of SpringOwl Asset Management, says that “most companies have adapted to changes that have been put in place in the UK, but we’re seeing a lot of UK business now go offshore. There’s been over regulation in the UK, and it’s pushed gaming to the black market. That’s unfortunate.”

As regulatory pressures increase, UK-listed gambling companies have been looking to offset these risks through international expansion. Entain has identified over 50 regulated markets across Central and Eastern Europe, Latin America and Africa where it currently has no presence, and the group recently completed the £316m takeover of Swedish sports betting and gaming company Enlabs, expanding its presence across the Baltics.

But the most significant opportunity is likely to lie in the US market, which Ader says “has the potential to be as big as the UK and EU combined.”

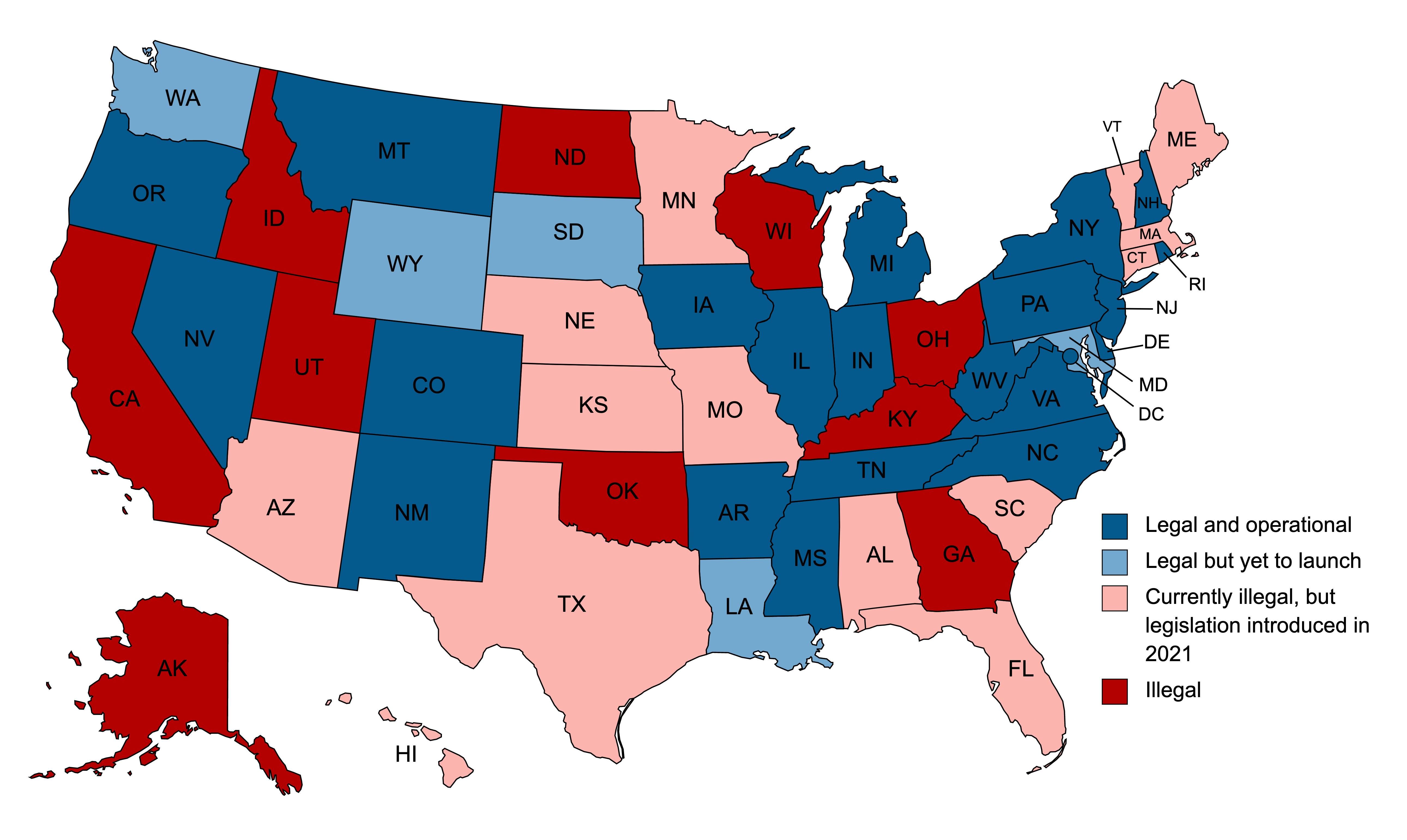

In 1992, the US passed the Professional and Amateur Sports Protection Act (PASPA), which essentially banned sports betting across the US in all but a handful of states. Nevada was the only state where all forms of sports betting were legal, while Delaware, Montana and Oregon permitted more limited formats.

This federal ban was overturned by a Supreme Court ruling in 2018, and individual states have since taken measures to make sports wagering legal. So far, 26 states and the District of Columbia have legalised sports betting, and for many of the remaining states, it seems to be a question of ‘when’, rather than ‘if’, they will follow suit.

The state of play: more US states are expected to legalise sports betting

Source: American Gaming Association

Map created using MapChart.net

Their efforts could accelerate in the wake of the pandemic. Russ Mould, investment director at AJ Bell, says that sports betting “could be a boon for cash-strapped states who are struggling to cope with the economic shock inflicted upon them by the pandemic. Some states charge hefty initial licensing fees and all will look to pocket taxes as a percentage of gross gaming revenue for good measure.”

That certainly seems to be the thinking in New York, where in-person sports betting is already permitted, but mobile wagering is set to be made legal.

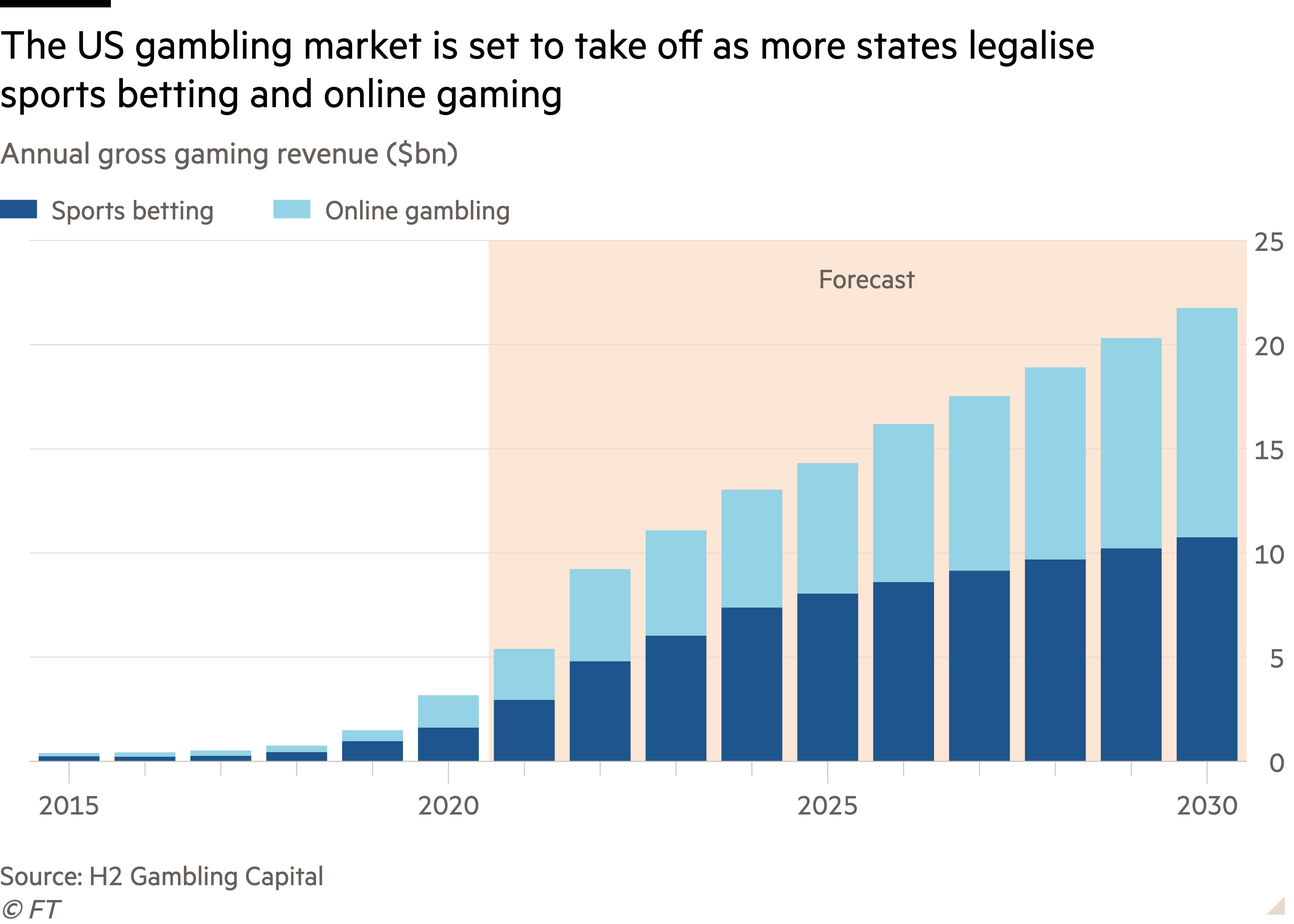

Analysts at Morgan Stanley predict that 39 states will have legalised sports betting by 2025, and that annual gross gaming revenue will reach $10.2bn (£7.4bn), up from $1.6bn in 2020. That’s a tantalising prospect, but cracking the US sports betting market isn’t without its challenges. In most instances, companies need to have a physical presence in a state in order to offer online sports betting. That’s why Entain set up a joint venture with MGM Resorts International (US:MGM), and William Hill (WMH) partnered with Caesars.

Online sports betting in the US is currently a loss-making business, as companies need to reach sufficient scale in order to achieve profitability. Flutter’s FanDuel platform and DraftKings (US:DKNG) are the leaders, with market shares of 35 per cent and 25 per cent, respectively.

While DraftKings started life as a fantasy sports app, it has expanded to cover real world live sports betting, offering a pureplay on online gambling. In the final quarter of 2020, the company increased its number of monthly unique players (MUP) by 44 per cent year-on-year, to 1.5m, and grew average revenue per MUP by 55 per cent to $65. Still, analysts believe profitability is still years away, although that hasn’t deterred several of Cathie Wood’s Ark Invest funds from building positions in the company, including the Ark Innovation ETF (US:ARKK).

Penn National Gaming is hoping to catch up with Flutter and DraftKings. It made a savvy purchase of a 36 per cent stake in sports media company Barstool Sports last year, looking to leverage Barstool’s brand and 66m monthly unique visitors. Penn has since launched its online sports betting market in three states, and while it is still early days, investors have lapped up the shares – they have risen more than sevenfold over the past year.

Amid the sky-high valuations, Ader says that the sports betting market could be “a bit of a Trojan horse for the casino industry. Online sports betting is not the greatest of businesses – it’s volatile and low margin.”

He sees more potential in states opening up to other modes of online gambling. “Sports betting is the easiest to move on first because it has widespread support from the leagues and municipalities,” says Ader. “But it’s going to be quickly followed by online gaming such as poker and bingo. Over the next 10 years you’re going to see a very broad suite of gaming offerings expanded online in the US, and the real profitability will be underneath sports, consistent with what you see in Europe and the UK.”

US gambling groups are comparatively inexperienced when it comes to online betting and sports wagering. As such, they have been looking to snap up UK operators as it is cheaper to acquire their technology and expertise than develop it from scratch.

Caesars struck an agreement for a £2.9bn takeover of William Hill last year. The deal is expected to complete shortly, although there could be a complication as hedge funds GWN Asset Management and HBK Capital Management are pushing for a new vote, arguing that shareholders were not given sufficient information prior to the original vote in November.

Meanwhile, Jackpotjoy-owner Gamesys (GYS) has reached an “agreement in principle” for a £2bn takeover by US casino operator Bally’s (US:BALY). Mould says that Gamesys’ “strong free cash flow, relatively lowly valuation and platform technology expertise will have all caught the eye of Bally, which will be looking to make the most of the deregulation of betting in America.”

Indeed, the tie-up would enhance Bally’s technology offering for online sports betting, while Gamesys would gain market access in the US. Bally’s has until close of play on 21 April to table a firm offer or walk away.

While the William Hill deal hangs in the balance, Peel Hunt believes that the Gamesys takeover will complete, and that 888 Holdings could be the next target. The broker says that “888 has the technology and knowhow to attract a takeover from any US company aspiring to US sports betting online gambling leadership.” Gambling software provider Playtech (PTEC) could also be a potential target.

MGM had been circling Ladbrokes-owner Entain for an £8.1bn takeover, but shelved its plans in January. Under Takeover Code rules, MGM can’t make another pass until July, and Ader says he wouldn’t be surprised if the companies do eventually agree to merge. “It seems like it’s a good strategic fit. Entain is very valuable. It’s a spectacular collection of assets and technology and MGM could very much benefit from owning it,” he says.

The regulatory threats to UK-listed gambling companies are not new, although it’s worth bearing in mind that a similar backlash could eventually unfold across the Atlantic as the US online market matures.

Excitement over US growth prospects is certainly not unfounded – further momentum will come as the normal sporting calendar resumes, states continue to liberalise and the e-sports industry also takes off. Even so, investors may have gotten a little ahead of themselves, with Flutter and Penn currently trading at a lofty 36 times and 45 times consensus 2022 earnings, respectively. Entain is more reasonably priced with a forward P/E ratio of 19 and it offers investors exposure to its US joint venture with MGM, which is currently operational in 12 states.